Fixing and flipping properties has enjoyed something of a golden era over the last two decades.

House fixing and flipping really started to pick up steam during the early 2000s, especially in the wake of the 2008 financial crisis. When housing prices plummeted, savvy real estate investors saw the opportunity to purchase properties at a discount, fix them, and sell them for a profit.

However, this is the 2020s, and the economy has changed. So, is fixing and flipping properties still a lucrative and sound investment in 2023?

The outlook for fix-and-flip properties in 2023

Some of the fundamental factors that affect how likely a fix-and-flip project is to succeed include local real estate market conditions, interest rates, the availability of financing, and your own financial goals and resources.

According to a March 2023 report by ATTOM Data Solutions, the average gross profit on a flipped property in the U.S. in 2022 was $67,900 in the fourth quarter of 2021, down from $70,000 in 2021. Here’s the thing, 2021 was the highest profit point since 2005, so there was bound to be a decline.

The average profit margin for flipped properties in 2022 was 26.9%, which factors the percentage of the property’s purchase price earned as profit after deducting the cost of renovations and other expenses.

That said, many real estate investors have earned significantly more or less depending on the project and the region of the country where their property resides. For a deal to be profitable, it’s essential for real estate investors to crunch the numbers to understand the cash-on-cash return before putting in an offer.

When you’re considering investing in fix and flip properties, the potential benefits haven’t changed:

Potential for profit

The profit potential still exists in the fix-and-flip market, especially with less competition in the market from potential homebuyers. When you can buy at a lower price and renovate a property to increase its value, you can sell it for a profit.

Active income

Fixing and flipping houses can provide an active source of income. And unlike passive investments, like stocks or mutual funds, you can actively control the outcome of the investment.

Potential tax benefits

Flipping houses can provide some tax benefits, such as deductions for renovation expenses and property taxes. As always, it’s essential to consult with a tax professional if you’re looking to fix and flip.

Diversify your real estate investment portfolio

Depending on the type of property and the scope of the work required to renovate and sell the property at a profit, fixing and flipping a property can bring in cash flow in a shorter amount of time than other types of real estate investments.

Potential pitfalls of fix and flip investing in 2023

While fixing and flipping properties can still be a lucrative investment strategy, there are also potential pitfalls to be aware of, especially in 2023, when the real estate market may experience changes due to economic, social, and political factors.

Here are a few potential pitfalls to keep in mind when deciding if a fix-and-flip project makes sense right now:

Market volatility

The real estate market can be volatile under the best circumstances, with prices fluctuating rapidly in response to economic and social changes. In 2023, in particular, adjustments to interest rates, inflationary risks, inventory issues, and economic uncertainty can impact the value of your property and potentially affect your profits.

Other factors, like the job market outlook and unemployment numbers, can also affect buyer behavior.

High competition

The popularity of fixing and flipping properties has led to increased competition among investors, which can drive up prices and make it harder to find good deals when buying diminished properties.

Rising construction costs

The cost of building materials and labor has been rising in recent years, which can increase the costs of renovating an investment property and lower your potential profit margin.

Regulatory changes

Government policies and regulations can change quickly and impact the real estate market in unforeseen ways. For example, changes to tax laws or zoning regulations can affect the profitability of your investment.

How interest rates affect the real estate market and your investments

Interest rates can significantly impact the real estate market, as they affect the cost of borrowing money to purchase or refinance a property. The fluctuation in interest rates can also impact how much buyers can spend on a new home.

It helps to understand the ways that changes in interest rates can impact the real estate market:

Affordability

New buyers are more likely to afford a home loan when interest rates are low, as lower interest rates mean lower monthly payments. Low interest rates, like those we’ve seen in the last couple of years, can increase home demand and drive up home prices. When interest rates are high, buyers are less likely to afford a new home loan, which can decrease demand for homes and drive down home prices — and potential profits for investors.

Refinancing

Changes in interest rates can also impact the number of people who refinance their home loans. When interest rates are low, many people refinance to take advantage of lower rates, which can stimulate the economy and increase consumer spending. When interest rates increase, fewer people are likely to refinance, which can slow down economic growth.

Overall, changes in interest rates can have a ripple effect on the real estate market and the general economy. However, as a fix and flip investor, you can refinance a short-term loan into a long-term loan to buy and hold until the market stabilizes.

2023 outlook

Spring is always the home-buying season. Because home inventory remains low, buyers are still looking for new homes.

As always, research the area you think you want to buy to find out how fast new and flipped homes are selling. Bargains still exist, and educated investors can take advantage.

The best tenant screening services enable landlords and property managers to run reliable credit history, criminal background checks, employment and income verification, and eviction history at fair rates. These platforms help protect your investments while saving time, money, and energy while looking for the right tenants. Depending on state laws, landlords can charge tenants for the application and background check fees to cover the cost.

We reviewed dozens of platforms to arrive at the top six best tenant screening services based on screening features, pricing, ease of use, customer support, and online reviews:

Buildium: Best overall for its comprehensive tenant screening services at affordable rates

Avail: Ideal for independent landlords who need free customizable screening reports and automated reference checks

RentRedi: Best mobile property management app for tenant screening

Apartments.com: Best free property management platform with auto-tenant screening feature and shareable tenant screening reports

TurboTenant: Recommended for independent landlords looking for free tenant screening service and free rental advertising

LeaseRunner: Great for small landlords who prefer flexible ala carte and individual tenant screening reports

Best Tenant Screening Services At a Glance

Tenant Screening Services

Tenant Screening Price

Free Plan

Mobile App

Customer Support

$15 per screening for landlordsor$30 per screening for applicants

Online tenant screening enables you to carefully filter applicants and find the best tenants faster through comprehensive credit history, eviction history, and criminal background reports. Take our quiz below to find the best tenant screening service for your rental business.

Buildium: Best Overall Tenant Screening Service

Overall Score: 5.00 / 5

What We Like

All-in-one property management solution

Supports multiple listing platforms

Tenant screening fees are more affordable than others on this list

No free plan

Expensive subscription rates

Phone support available in more expensive subscriptions

Website chat support is handled by a chatbot instead of a live person

Why should you choose Buildium?

Buildium is highly recommended for landlords with multiple properties of up to 5,000 units (or more). As a tenant screening service, Buildium helps you get access to comprehensive credit, criminal, and eviction history reports. Its tenant screening services are relatively cheaper than similar providers, especially when shouldered by the landlord.

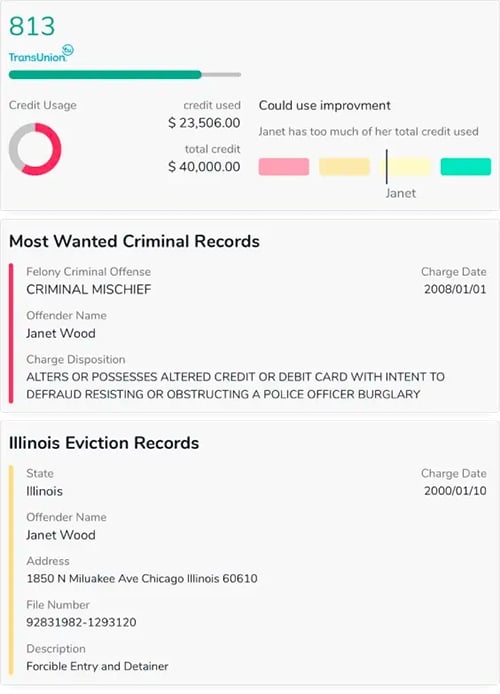

Buildium is our best overall screening service because of its comprehensive software features, affordable tenant screening reports, and all-in-one property management solution. Powered by TransUnion, a US credit reporting agency, landlords can access full credit, criminal, and eviction data to help them avoid tenant scams. You only need to make a request and set custom requirements, and Buildium will begin tenant credit and background checks for you.

Landlords have two screening options: basic and premium. Unlike basic tenant screening, the premium option allows for customized thresholds on recommendations, requires minimal applicant involvement, and delivers faster results. Both tenant screening plans include rental recommendations from TransUnion, a full credit report, identity verification, eviction history, and background check for renters.

Buildium will automatically send tenants a reminder to complete the rental application at the three-day mark and the seven-day mark after the process begins. If you’re still considering your options, take advantage of Buildium’s 14-day free trial, allowing you to experience the platform before committing to a subscription.

Additional Buildium Features

Tenant screening criteria: set minimum credit score and other qualifying questions in the application form like pets, move-in dates, and deposits to easily filter qualified from unqualified applicants and stay aligned with landlord-tenant laws

Property management: includes several property management functions, such as accounting, maintenance, tasks, violations, resident and board member communications, and online portals

Marketing website: a do-it-yourself, free, fully integrated website for property managers, hosted by Buildium

eSignatures: manage all leasing processes online and get documents signed digitally

Performance and business analytics: receive insights into your residents’ activities through the resident center and a detailed analysis of your business performance using key leasing metrics

Buildium Customer Feedback

Customers rated Buildium 4.5 out of 5 because of its robust platform and multiple tools available for property management. They also like the ability to switch between different properties in their portfolio. One client said the property management automation helped them save time and money. Landlords also praised Buildium’s customer support for its professional assistance.

In less positive Buildium reviews, a client found the lease processing procedures in the basic plan complicated. Another client said it was difficult to set up the late fee charge and thought the settings for late fees were too limited. Buildium doesn’t have a free plan, and its plans are more expensive than other software on this list. If you’re managing a few properties and want to try a free property management service, we recommend Avail.

Buildium Pricing

Buildium offers tiered subscription plans that include basic and premium resident screening services. In the basic tenant screening, landlords have the option to cover the cost of screening themselves or pass the cost on to the applicant. With basic tenant screening, landlords pay $15 per screening or $30 if paid by the applicant, whereas the premium screening is $18 per screening.

Aside from paying the tenant screening service fees, Buildium account holders also need to pay a monthly subscription. Check out its plan inclusions below:

Essential: starts at $50, paid monthly; this includes basic tenant screening, rental accounting, maintenance, tasks violation, ticket support, and online portals.

Growth: starts at $160, paid monthly; aside from features included in the Essential plan, users also get premium tenant screening, unlimited e-signatures, five free bank accounts, standard reports, performance, business analytics, and live phone support.

Premium: starts at $460, paid monthly; includes everything in the Growth plan, plus open API, Buildium Rewards, priority support, and a dedicated growth consultant.

Avail: Best Free Customizable Tenant Screening Service With Automated Reference Checks

Checks

Overall Score: 4.88 / 5

What We Like

Option to pass on tenant screening fees to applicants

Comprehensive and customizable tenant screening reports

Applicant communication and message center available on the platform

Free subscription plan

No mobile app

Tenant screening fees may vary by location

Website chat support is handled by a chatbot instead of a live person

Why should you choose Avail?

Avail is best for small and mid-sized landlords looking for a free property management platform with affordable tenant screening services and automated reference checks. While tenant screening reports are not free, landlords can choose to pass on these fees to the applicant.

If you’re looking for free property management software with customizable renter reports, we recommend Avail. It provides online tenant screening services, focusing on background and credit checks for landlords—whether you need a TransUnion report, national criminal history, prior eviction data, or a complete tenant background check. Landlords could also customize application settings and screening questions to make sure tenants qualify for all their requirements.

Another unique feature of Avail is its automated reference checks. Once prospects complete the online renter application form, Avail automatically contacts their previous landlords to see whether they paid their rent on time and took care of the rental property. The platform also enables landlords to conduct income verification and documentation to ensure prospects are able to pay the rent on time.

Unlike most service providers on this list, Avail has a free subscription plan where landlords can enjoy comprehensive property management features, such as syndicated listings, online rent collection, and maintenance tracking at no cost to them. It also helps landlords streamline their communication with existing tenants in one software.

Additional Avail Features

Sample Tenant Screening Report (Source: Avail)

Rental listings: create one rental listing to post across multiple sites, such as Realtor.com and Trulia, with one click

Digital leases: access lawyer-reviewed, state-specific lease agreement templates, including all the necessary disclosures, attachments, and clauses

Online rent collection: allow tenants to pay rent online, schedule upcoming payments, issue late fees, track rental income, and get paid faster with Avail’s FastPay

Maintenance tracking: track repairs with in-app messaging, photos, and automatic maintenance records

Rent price analysis: complete rental market trends and rent comps so you can set competitive rent prices

Avail Customer Feedback

Avail’s subscribers praise the platform for its ease of use, affordable pricing, and superb customer support, giving it a 4.6 out of 5-star review. One user said that Avail made the background and rental credit check, as well as communicating with applicants, easy. One property manager enjoyed the syndication between all the websites when listing available units, which helped him find tenants faster.

While most reviews are positive, some experienced glitchy features, lags on the screen, and other technical issues. Avail doesn’t currently have an app, which could be inconvenient for landlords who are always on the go. If you’re looking for a property management app with a mobile tenant screening feature, check out RentRedi or Buildium.

Avail Pricing

Avail offers two subscription plans: unlimited free and unlimited plus. Both subscription plans include tenant screening services that you can purchase ala carte or as a bundled package. The price of each screening report varies depending on the state but may start from $30 each or $55 for bundled packages. Landlords can pay the fees themselves or pass them on to the applicant.

To see which Avail subscription plan is perfect for your business, check the table below:

Unlimited Free: free; includes syndicated listings, credit and criminal screening, state-specific leases, online rent payments, and maintenance tracking

Unlimited Plus: Starts at $7 per unit monthly; includes everything in the Unlimited Free plan plus next-day rent payments, waived ACH fees, custom applications and leases, clone and reuse custom lease agreement, and create a properties website

RentRedi: Excellent for Mobile Tenant Screening Process

Overall Score: 4.82 / 5

What We Like

Auto-tenant screening feature

More affordable tenant screening service than other platforms

Multiple renewal subscription options

Free listings on Realtor.com and Doorsteps

No free trial and no free subscription plan

No tiered plans with ala carte features

No automated reference checks

Why should you choose RentRedi?

RentRedi is perfect for small to mid-sized landlords who are always on the go. With RentRedi’s robust mobile app, you can easily send tenant screening requests and have the applicant approve the request on their phone.

RentRedi is perfect for landlords who want the convenience of mobile technology when screening applicants. Landlords can send requests, view screening reports, and accept applications directly on the mobile app—no need to log in and out on a web browser. As a tenant screening service, RentRedi provides full credit, criminal, and eviction reports. RentRedi also has an auto-tenant screening feature, which allows landlords to automatically receive a completed tenant screening report once a prospect submits an application.

To run a credit background check for tenants, RentRedi has partnered with TransUnion and uses ResidentScore, which predicts rental eviction risk 15% better than traditional credit scores. It also reviews over 370 million records from state and national databases to make sure you get a thorough criminal report. Additionally, RentRedi checks 27 million eviction records through a large eviction database subject to The Fair Credit Reporting Act (FCRA), which covers all 50 states.

RentRedi has other key features that allow you to automate your rental processes such as online rent collection and accounting, tenant prequalifications and applications, maintenance requests and coordination, listing syndications and advertising, and tenant and team communications. These features help landlords protect their real estate investments, filter the right applicants, and manage existing tenants.

Additional RentRedi Features

Rent collection: tenants can send money via credit card, ACH, cash, and banking. Landlords receive payments within three to four business days and can export payments to spreadsheets or QuickBooks

Prequalifications and applications: set prequalification questions to immediately determine whether an applicant qualifies or not before scheduling a tour

Maintenance requests and coordination: outsource managing maintenance requests and get automatic maintenance status updates sent to the tenant

Listings and marketing: free Realtor and Doorsteps listing syndications using the RentRedi dashboard; add virtual tour options to property listings and have a free professionally designed marketing page to share on your websites and other marketing sites

RentRedi Customer Feedback

Customers enjoy using RentRedi because of its easy setup and responsive customer support. Landlords found the mobile app very convenient and user-friendly, especially the ability to properly screen applicants, collect rents, notify tenants, and respond to maintenance requests directly on their mobile phones. Because of these reasons, RentRedi received a 4.5 out of 5-star rating.

While most customers found RentRedi helpful and convenient, a few customers said they don’t use some of the features included in their subscriptions. This is not cost-efficient since subscribers pay a flat monthly or annual fee. Some also experienced technical and update issues with the mobile app. If you’re budget conscious and prefer to purchase ala carte features instead, check out LeaseRunner.

RentRedi Pricing

Landlords can enjoy RentRedi’s property management features, including tenant screening, by paying a monthly subscription fee of as low as $9 monthly. Prospective tenants will also have to pay $35 for the rental background check.

Apartments.com: Recommended for Free Auto-tenant Screening Feature & Shareable Reports

Overall Score: 4.73 / 5

What We Like

All-in-one property management platform with an auto-tenant screening feature

Comprehensive tenant screening reports

Screening reports are shareable up to 10 participating landlords

No mobile app features available for property managers

Subscription plans and premium pricing are not disclosed on the website

No live chat support

Why should you choose Apartments.com?

Apartments.com is ideal for independent landlords looking for free tenant screening services and free rent collection software. Once prospective tenants apply for your rental property, they will be required to pay an application fee, covering their credit, eviction, and criminal reports.

If you need fast and easy access to tenant screening reports when an applicant clicks the “Apply” button on your listing, we recommend using Apartments.com. Once a renter applies to your listing, they must pay $29 to run their TransUnion credit, criminal, and eviction reports online. Another unique feature of Apartments.com is that it allows an applicant’s screening report to be shared with other participating rentals on the site. The tenant’s application can be used for up to ten (10) different listings and is valid within 30 days.

While the screening reports are free to the landlord, applicants need to pay for their reports once they apply for your property on Apartments.com. This reduces the financial burden on landlords. However, landlords have the option to pay the application fee if they prefer. The applicant’s data are also securely stored online so landlords can access it wherever they are.

Apartments.com is also an all-in-one suite of property management tools that make the rental process paperless and more convenient for landlords and renters. Aside from screening tenants, Apartments.com allows you to list your property, receive applications, generate a lease, collect payments, manage residents, organize expenses, and track maintenance from anywhere with a reliable internet connection.

Additional Apartments.com Features

Auto-tenant screening: get detailed renter information, including income-to-rent-ratio, employment status, household info, and rental history, once applicants submit their application through your Apartments.com listing

Property listings and virtual tours: list your properties on Apartment.com and conduct property tours online and from anywhere

Online lease agreements: creating state-compliant online lease agreements customized to your locale; both you and the tenants can sign the lease documents with an e-Signature and access documents online

Resident management: keep and access all of your tenants’ relevant information securely in one centralized location; share documents with tenants online

Expense tracking: organize, track, and export your rental property expenses from anywhere to make tax preparation easier

Maintenance requests: receive and manage maintenance requests directly from tenants on your online dashboard

Apartments.com Customer Feedback

Apartments.com received mixed reviews, giving it an average 3.9 out of 5-star review. Loyal customers who have been using Apartments.com for several years love the platform for its rental advertising and online rental collection features. A landlord also appreciated that Apartments.com allows interested tenants and existing renters to communicate with them directly by sending messages and requests on the platform.

Some landlords complained of expensive premium rental advertising. A customer also found the platform’s back-end “cumbersome to make corrections or changes to a listing.” Furthermore, property managers are currently unable to utilize the mobile app, which means they have to log in to their accounts through a web browser to update and maintain listings. If you’re looking for a free tenant screening service with a mobile app, check out RentRedi and TurboTenant.

Apartments.com Pricing

Apartments.com’s tenant screening feature is free for landlords. Applicants, however, have to pay $29 (plus tax) for their application and screening reports. The application is reusable, and screening reports can be shared with up to ten (10) participating Apartments.com landlords for 30 days.

TurboTenant: Best Free Tenant Screening Services & Free Rental Advertising

Overall Score: 4.10 / 5

What We Like

Free software version without trial limit

Comprehensive tenant screening reports

Past landlord references

Mobile app

No phone support available for free subscribers

Tenant application fee more expensive than other tenant screening services

Rental accounting feature available as an add-on service to any subscription plan

Why should you choose TurboTenant?

TurboTenant is great for independent landlords who need an easy-to-use and free software platform to manage their rental properties and find good applicants. Its free tenant screening feature provides you with complete credit, criminal, and eviction reports, as well as past landlord references. It also allows you to market your rental vacancies, receive online applications, accept rent payments, track expenses, and even manage maintenance requests for free.

For property managers looking for free property management software, TurboTenant gives you a complete snapshot of a prospective tenant’s financial stability and credibility through a quick and easy tenant screening process at no cost to you. In partnership with TransUnion, landlords can run a comprehensive credit report that includes debt payment history, new loans, history of bankruptcies, and even late payments in their rental history.

TurboTenant also helps you gain insights into their previous rentals and landlords, as well as verify their income and employment. The software searches over millions of criminal records across the country, so you know if an applicant might pose any threat to your business and other tenants. Furthermore, landlords will get a detailed report of past evictions of a would-be renter.

Aside from tenant screening, TurboTenant helps landlords stay organized through its other property management features, including rental marketing, lease agreements, document management, rent collection, maintenance requests, and expense tracking. These features are free to use for landlords, with premium upgrades available.

Additional TurboTenant Features

Rental advertising: advertise properties for free on multiple rental listing websites like Realtor.com, ApartmentList, Rent.com, and Craigslist; create professional listing pages for your properties

Lease agreements: customize a state-specific online lease agreement crafted by local lawyers and expert landlords

Rent payments: securely collect rent online, connect your bank account, and set up automatic monthly charges and late fees

Maintenance requests: manage and keep track of tenant requests online

Expense tracking: organize and monitor your expenses in a purpose-built software and export them as a CSV file when filing taxes

TurboTenant Customer Feedback

TurboTenant’s customers love the platform because of its free features with upgrade options and responsive support staff. Another customer loved its all-in-one property management solution that enables them to advertise their properties across multiple sites, communicate with potential tenants, pre-screen and screen applicants, and accept applications.

On the other hand, some customers complained of having issues with their accounts, like suddenly blocked or suspended accounts. Others also don’t like the long period of time it takes for their tenants’ rents to be deposited in their bank accounts. TurboTenant’s screening fees can also be more expensive than others on this list. Because of these mixed reviews, TurboTenant received a 3.7 out of 5-star review. For more affordable options, check out Avail, Apartments.com, or LeaseRunner.

TurboTenant Pricing

Using TurboTenant’s tenant screening feature is free for landlords, although tenants have to pay $55, which covers the application fee and tenant screening reports. You can choose to pay the fee yourself if you prefer or if you’ve already collected an application fee from the applicant. TurboTenant also has free and premium subscription plans that give you access to multiple property management features.

Free Plan: free; includes unlimited properties, rental advertising, lead management, applications and screening, automated reference checks, rent payment, expense tracking, maintenance requests, messaging, document management, chat support, and one connected bank account

Premium Plan: $4.92 monthly; includes everything in the Free Plan plus expedited rent payouts, connected bank accounts, state-specific lease agreements, lease addendums, e-signatures, and landlords forms pack

LeaseRunner: Best for Its Ala Carte Tenant Screening Reports

Overall Score: 3.98 / 5

What We Like

Customizable tenant screening report

Free online rental application form

No monthly subscription fees

Mobile app

No bundled packages

No live chat support

Total cost for complete tenant screening reports is more expensive than other services

Why should you choose LeaseRunner?

LeaseRunner is ideal for landlords managing a few properties and who want to run individual tenant screening reports. For instance, if you only need a credit score report, you don’t have to pay for criminal and eviction history records if you don’t need them. Its ala carte features also enable landlords to automate certain property management processes like rent collection and digital lease with e-signatures.

For independent landlords managing a few rental properties, LeaseRunner is a practical choice because of its flexible pricing and ala carte tenant screening menu. LeaseRunner has no subscription and monthly fees. Instead, you can choose the type of service you want. This allows you to mix and match tenant screening reports based on your preference, local rental market, and ideal renter’s profile, and pay only for what you really need. For example, you can request a criminal background check but not a credit check, or vice versa.

LeaseRunner has an extensive selection of screening services, including tenant criminal background, credit record, financial profile, and eviction history reports. It has advanced applicant record matching and compares over 36 million eviction records, 300 million credit records, 500 million criminal records, as well as credit, court, government, and bank data.

LeaseRunner also has other features that help landlords automate their rental processes. It offers free rental application form templates, paperless state-specific lease agreements with e-signatures, ACH (Automated Clearing House) online rent collection, and rental ad tools. The platform also has 5,400 bank integrations. What’s more, LeaseRunner is fully optimized for mobile use and is compliant with Fair Housing Act making it a convenient and secure property management platform for small landlords.

Additional LeaseRunner Features

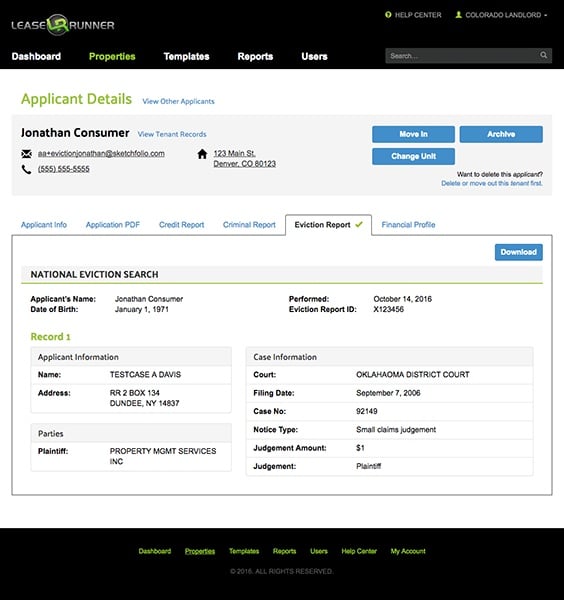

Sample Eviction History Report (Source: LeaseRunner)

Applicant authorization: applicants can authorize the release of their credit, financial, eviction, and criminal records from their email and don’t need to create a LeaseRunner account or go to the website.

Rental ads: post rental listings to multiple sites like Facebook, Twitter, and Craigslist and generate application buttons and links

Digital rental application: email the application link to tenants so they can apply online or via smartphone

Digital lease with e-signature: compile multiple documents and email them for e-signature

Online rent payment: collect rent and fees by bank debit through the Tenant Payment Center or autopay

LeaseRunner Customer Feedback

Landlords who use LeaseRunner like the platform for its inexpensive and easy-to-use features, giving it a 4.6 out of 5-star review. One customer even commented that it is “the easiest tenant application and screening process for landlords.” Another praised the platform because it made listing, creating, and signing leases easy. A loyal customer of ten (10) years particularly liked that LeaseRunner allows tenants to accomplish an application for free and conduct the background and credit check separately if they decide to move forward.

While customers find the platform useful, one customer commented on LeaseRunner’s “buggy” software. Another landlord complained of receiving incomplete information on an applicant’s credit score and financial profile. Further, LeaseRunner does not offer packages, and the total cost of its complete tenant screening report can be more expensive than other tenant screening services. If you’re an independent landlord with few properties, you can check Avail’s monthly free and affordable subscription plans.

LeaseRunner Pricing

LeaseRunner can provide you with detailed tenant reports at competitive rates. Unlike other tenant screening services on this list, landlords can choose to only pay for individual background reports for $10. However, if you need complete tenant screening information, the costs would amount to $60, which is more expensive than other services. Below are the prices of each type of tenant screening report:

How We Evaluated the Top Tenant Screening Services

To determine the best tenant screening services, we evaluated platforms based on features related to comprehensive and reliable background checks and identity verification. The pricing structures were also compared, so property managers and landlords know which service is right for their budget. We also reviewed each platform’s ease of use and available customer support, which are essential to successfully screen tenants in the most efficient way possible.

Based on our evaluation, Buildium is the best tenant background check company that provides comprehensive tenant screening reports at more affordable rates than others. Landlords can easily run a renter’s check, including credit history, criminal background, and eviction report, from anywhere with an internet connection. Buildium also provides an all-in-one property management solution with features like online rental listings and marketing, real estate accounting, rent collection, and maintenance requests.

Below are the criteria we used to determine the top tenant screening companies for landlords and property managers.

Screening tenants for a rental property is a critical process that can significantly impact a property’s success and profitability. By implementing effective screening methods, landlords can attract reliable and responsible tenants who will not only meet their rental obligations but also help property owners maximize the potential of their investment. In this article, we explore seven key steps in screening tenants to ensure landlords make informed decisions to fill their vacancies while adhering to Fair Housing Laws.

Property owners should plan ahead by utilizing a tenant screening checklist to guarantee they’ve covered the necessary steps in the tenant screening process. Download our complimentary checklist and decision flowchart below, which includes rental application items, ways to verify income and employment, and tenant interview questions.

1. Understand & Comply With Fair Housing Laws

It is important to have a comprehensive understanding of Fair Housing Laws before embarking on the apartment screening process. Familiarize yourself with federal, state, and local regulations to ensure compliance and to help you avoid any discriminatory practices. Landlords must treat all applicants fairly and equally, without any bias based on race, color, religion, sex, national origin, familial status, or disability.

To avoid breaking fair housing laws, landlords should follow these general guidelines:

Treat all applicants equally: Treat every applicant fairly and equally regardless of their background or characteristics. Avoid any form of discrimination or bias during the process of screening tenants.

Use consistent screening criteria: Develop a clear set of qualifications and requirements based on factors like income, rental history, creditworthiness, and references. Apply these criteria uniformly for all applicants and avoid making exceptions for specific individuals or groups.

Advertise responsibly: When advertising your rental property, avoid any language, images, or statements that could be interpreted as discriminatory. Focus on describing the property features, amenities, and location rather than using language that targets specific groups of people.

Ask legal and objective screening questions: During interviews or interactions with applicants, ask only legal and objective screening questions directly related to their qualifications as tenants. Avoid inquiries about protected characteristics, family status, and disabilities.

Maintain accurate records: Keep detailed records of all interactions, communications, applications, and screening results. Documentation can help demonstrate that your tenant selection process is fair and unbiased.

Use screening services: Utilize reputable tenant screening services or credit reporting agencies to conduct credit checks and background checks during the verification processes. These services are equipped to handle sensitive information and ensure compliance with fair housing laws.

2. Use a Rental Application to Prescreen Tenants

Utilizing a well-designed rental application is a practical step in the tenant screening process to protect your investment properties. A comprehensive application helps gather essential information like personal details, employment history, income verification, references, and consent for background and credit checks. The application acts as a prescreening tool, allowing you to screen tenants and determine their suitability for your rental property.

A rental application should include several key pieces of information to help landlords assess the fit of potential tenants. Here are some essential details that should be listed on your application:

Personal and contact information: The application should require the applicant’s full name, current address, phone number, and email address. This information allows landlords to contact applicants and verify their identity.

Employment history: Requesting details about the applicant’s employment history, including current and previous employers, job titles, and durations of employment, helps assess their stability and income source. This information offers insights into their ability to meet their financial obligations.

Income verification: A rental application should include a section where applicants can provide proof of income, such as recent pay stubs, employment contracts, or tax documents. Verifying income ensures that tenants have the financial means to pay rent consistently.

References: Applicants should be asked to provide references from previous landlords or professional contacts who can vouch for their character and reliability. Contacting references offers valuable insights into the applicant’s rental history, payment habits, and general conduct as a tenant.

Rental history: It is important to gather information about the applicant’s previous rental history, including addresses of previous residences, dates of tenancy, and reasons for moving. This allows landlords to assess their rental track record and helps landlords understand where their tenant has lived and in what types of properties.

Consent for credit and background checks:Including a section where applicants grant consent for credit and background checks is crucial. This authorization enables landlords to request personal information on the tenant from the right legal entities.

Additional information: Depending on specific preferences or property requirements, the application may include additional sections, such as questions about pets and vehicle information, or ask any specific questions that might help in determining their eligibility.

3. Run a Credit Report & Background Check

Once you’ve obtained a completed rental application, you can run a credit and background check on the tenant. A credit report serves as a valuable resource for landlords by providing essential information that helps assess the financial responsibility and reliability of prospective tenants. This detailed evaluation allows landlords to gauge an applicant’s ability to meet financial obligations, including paying rent on time.

A background check is a valuable tool that landlords can utilize to gain insights into a prospective tenant’s history. By conducting a background check, landlords can uncover crucial information to help you make informed decisions during the tenant screening process.

Key information that will be found on a prospective tenant’s credit report and background check are:

Credit score: The credit score provides an overall snapshot of their creditworthiness. A higher score typically indicates a more responsible approach to managing financial obligations. Most landlords like to see a score of 700 or above.

Payment history: In the applicant’s payment history, landlords can look for patterns of late payments, delinquencies, or accounts in collections. Consistent on-time payments demonstrate a tenant’s financial responsibility.

Debt-to-income ratio: The debt-to-income ratio indicates their level of financial obligations compared to their income. A lower ratio suggests a better ability to manage additional rental expenses.

Outstanding debts: Look for any outstanding debts or judgments against the applicant, as these may affect their ability to pay rent consistently.

Criminal records: Check for any criminal records or convictions. While minor offenses may not be immediate grounds for rejection, serious offenses should be carefully evaluated.

4. Verify Income & Employment

Verifying income and employment helps landlords select tenants with the financial stability to fulfill their rental payments. Landlords should have a general guideline for income requirements needed from tenants. A common guideline often followed by landlords is the “three times the monthly rent” rule.

This means that applicants are typically expected to have a monthly income that is at least three times the amount of the monthly rent. For example, if the monthly rent is $1,500, applicants would generally be expected to have a minimum monthly income of $4,500.

However, you can choose to increase or decrease this multiple. For example, in New York City, tenants are required to make 40 times the rent to qualify for an apartment. So, if you want to rent a $2,000 apartment, you must make $80,000 per year.

Some landlords may have higher or lower income requirements based on their specific circumstances and preferences. Landlords can verify income and employment by contacting employers, requesting pay stubs, and employment contracts, or using professional verification services like RentPrep. Check out our RentPrep review if you’re interested in learning more about this tool.

5. Check Previous Addresses, Landlord & Eviction History

In addition to verifying income, when learning how to screen tenants for rental property, it’s essential for landlords to verify an applicant’s previous addresses and landlord and eviction history. Thoroughly vetting application information increases confidence that the applicant meets your rental qualifications and will be a good tenant.

By asking for references and rental history information on the tenant application, landlords can uncover information about a prospective tenant’s previous addresses, eviction history, and former landlord relationship status. Details you want to discuss with a tenant’s former landlord are payment history, adherence to lease terms, property maintenance, behavior as a tenant, and any issues or disputes during the tenancy.

When contacting a tenant’s former landlord, consider asking the following questions:

Can you confirm the applicant’s tenancy at your property?

How long did the applicant reside at your property?

Did the applicant consistently pay rent on time? Were there any instances of late payments?

How would you describe the applicant’s communication and cooperation during their tenancy?

Did the applicant maintain the property in good condition?

Were there any reported issues or complaints from neighbors or other tenants related to the applicant?

Did the applicant provide proper notice when planning to move out?

Were there any lease violations, disputes, or conflicts during their tenancy?

Would you consider renting to this applicant again in the future?

Landlords can offer tenants an easy way of paying their monthly rent online to guarantee on-time payments with Baselane. Tenants can easily submit rent payments online, eliminating the need for paper checks or in-person transactions. This streamlined approach not only saves time but also ensures timely and consistent rent collection. Additionally, Baselane provides landlords with financial management tools to allow them to track income, expenses, and quickly generate detailed financial reports.

6. Interview Applicants & Ask Screening Questions

Once you’ve reviewed all application information and you’ve determined that you would like to proceed with a prospective tenant, then conducting face-to-face or virtual interviews with applicants may help you finalize your decision.

Landlords should prepare a list of questions when screening potential renters. These questions should be tailored to your specific requirements, covering rental preferences, lifestyle, and ability to meet rental obligations. Observe their communication skills, professionalism, and general demeanor during the interview to gauge compatibility.

Here are some suggestions for what landlords can do during the interview process and sample questions they can ask to assess if the tenant will be a good fit:

Example Questions You Can Ask

Example Questions You CANNOT Ask

Do you have any pets?

Do you have any medical conditions?

Are you willing to comply with the property’s rules and regulations?

What is your sexual orientation?

Can you pay the lease application fee?

Do you have any plans to start a family?

Have you ever broken a rental agreement?

Are you married or single?

Are you able to meet the monthly rent obligations?

Do you have a

7. Accept or Reject the Applicants After Screening

After carefully evaluating each applicant’s qualifications and determining whether they align with your renter criteria, landlords must decide whether to accept or reject their tenant’s application. Landlords should base their decision on a tenant’s creditworthiness, rental history, income stability, and overall compatibility to make an informed decision. Communicate your decision promptly and in compliance with applicable laws and regulations.

To help with the evaluation process, landlords should develop a clear set of screening criteria to objectively evaluate potential tenants. This is especially helpful when you have multiple applications, and you need to pick the applicant best fit for your property. Some screening criteria to help you with accepting the right tenant:

Sufficient income: The applicant should have income that meets or exceeds the requirement of three times the monthly rent.

Stable employment: A stable work history shows a continuous duration of time in their current job. This indicates reliability and a higher likelihood of consistent income.

Verifiable income: Verify the applicant’s income through their current employer documents or tax returns. This helps confirm their financial stability and ability to meet rental obligations.

Satisfactory credit: Assess the applicant’s credit history to make sure they have a strong credit profile. This indicates responsible financial behavior and increases the likelihood of timely rent payments.

Clean criminal background: Check for a criminal background free of felonies or misdemeanors to prioritize tenant safety and security.

Positive rental history: Evaluate the applicant’s previous residence and landlord history for a favorable track record of fulfilling lease obligations and maintaining their past properties.

After you determine whether the prospective tenant meets your criteria, you will be able to either accept or reject their application.

Tools to Assist With Screening Tenants

Landlords can leverage advanced software to screen prospective tenants. These tools offer a variety of features like automated rental applications, online background checks, and credit assessments. By using tools throughout the tenant screening process, landlords can save time, reduce manual paperwork, and make data-driven decisions. This ultimately helps with selecting the most qualified and reliable tenants for your rental properties.

Bottom Line

By taking the time to learn how to screen tenants in your property will reduce the headache of having to evict a bad tenant in the long run. Landlords should implement a thorough tenant screening process to minimize potential tenant scams, secure responsible tenants, and foster a positive landlord-tenant relationship. Leveraging technology and software tools can streamline the screening process and provide valuable insights into prospective tenants.

Several individuals want to get involved in real estate investing but are reluctant to take the leap. These people are ready to leave their nine-to-five job to pursue a life of financial freedom. Still, they are unaware of the sources to finance a real estate business. Many assume if they don’t have capital of their own, it is impossible to get started. However, this rationale is false.

There are a variety of ways to finance a real estate business without using your own money. Not only are there real estate development loans, but there are plenty of private lenders out there willing to take a risk on your business. If you desperately desire to leave your day job so that you can prosper as an entrepreneur, consider property development loans.

What Are Real Estate Development Loans?

Real estate development loans are capital advancements issued to borrowers who need funds to break ground on a project, build, and hold the finished product through the leasing stage. Investors typically rely on real estate development financing to do one of two things: buy raw land to eventually build on or tear down an existing building, only to build a new one.

4 Types Of Real Estate Development Loans

The most popular types of real estate development loans include, but are not limited to:

Acquisition Loans

Development Loans

Acquisition And Development Loans

Construction Loans

Acquisition Loans

As their names suggest, acquisition loans are specifically used to finance the purchase of undeveloped land. Acquisition loans will often be used to buy land with no intentions of developing on it. While common, acquisition loans provide little room for action and must typically be accompanied by subsequent loans to develop the land further. Of the real estate development loans made available to investors, this offers the least amount of freedom.

Development Loans

If borrowers want to develop the land they recently acquired, they may need a loan to move forward with any plans. Development loans are traditionally borrowed to do just that. Borrowers will take out development loans to make improvements on the land. Leveling, building roads, and running water lines may all be accomplished by taking out a development loan. On top of that, development loans are necessary to turn raw land into a building site.

Acquisition And Development Loans

Sometimes borrowers want to both acquire raw land and develop it at the same time. Fortunately, there’s a loan for that: acquisition and development loans. As their names suggest, these loans enable borrowers to buy raw land and turn it into a building site. OF the real estate development loans made available, this one is the most versatile.

Construction Loans

Construction loans — not surprisingly — are used to finance the building or renovation of a respective real estate project. According to Links Financial, “it differs from other loans in that the developer receives the money in monthly draws as development progresses rather than in one lump sum at the beginning of the project. Monthly loan payments increase as you draw out more money.”

What Is The Capital Stack?

The capital stack is the various layers of financing used to make up a project. In the real estate industry, it’s common, if not expected, to rely on more than one source of funding when acquiring a deal. Each loan makes up the resulting capital stack, with high priority funding sources on top and more senior debt on the bottom. In financing, the capital stack is made up of senior debt, mezzanine debt, preferred equity, and common equity.

The bottom of the capital stack, or senior debt, is typically the highest priority but lowest risk debt. These are typically loans that are secured by the property. At the top, is common equity which is considered the lowest priority or highest risk debt. These loans are only repaid when the rest of the capital stack has been repaid. Essentially, this concept is used to prioritize the different financing methods that go into a real estate deal.

11 Real Estate Funding Sources

There are several sources to finance a real estate business, but the most popular of them all are listed below:

Traditional Loans: Traditional loans are those you would receive from a bank or an institutionalized lender. Their interest rates are relatively low in an attempt to remain competitive. However, their lengths are typically long, and their underwriting is extensive. Most traditional loans last anywhere from 15 years to 30 or more and come with an interest rate somewhere in the neighborhood of four percent.

Private Lenders: Private lenders can be anyone with access to capital and a willingness to invest it. In other words, private lenders can be anyone from a close friend to someone you met at a networking event. As their names suggest, private lenders are not institutionalized or licensed to lend money but rather do so to make their money back with interest. Private lender terms are typically easier to meet, and the duration in which they are willing to lend will be much shorter, but at the cost of an interest rate around 12 to 15 percent.

Venture Capitalists: Venture capitalists are high-net-worth individuals or corporations who tend to invest in startups that have shown potential. Venture capitalists are often willing to lend far more than a traditional small-business loan, but their selective nature can be harder to receive approval.

Angel investors: Angel investors are usually well-off individuals who provide funding for new business ventures, typically in exchange for convertible debt or ownership equity. Angel investors have developed a reputation for taking more risk, but it’s important to note the money from an angel investor isn’t technically a loan. The money represents the acquisition of part of the business.

Small business administration loans: Small business administration loans are issued by the government in a variety of packages. Small business loans offer many options, but they can be tedious to apply for and are not quick to receive.

Real estate crowdfunding: Real estate crowdfunding is a process that involves pooling together funds from multiple sources and people. Crowdsourcing can offer recipients flexible terms and is growing in popularity.

Microloans: Microloans offer small business owners to $50,000, though most people tend to take much less than that. Due to their size, small business loans are typically easier to obtain than a traditional loan, but there’s a chance the loan doesn’t cover all of your needs.

Hard money lenders: Hard money lenders are not institutionalized, but they may be licensed to lend money. Their loan terms are typically short and leveraged with the asset in question. Hard money loans come with a high interest rate, often around 12 percent, but they can give borrowers access to capital fast.

Home equity loans and lines of credit: Home equity loans and lines of credit, or HELOCs as they are known, represent a type of revolving credit—not unlike a credit card. Home equity loans, however, use the equity in your home as collateral.

Money partners: Money partners are just that: individuals who you may partner up with because of their access to funding. If you don’t have access to capital, it may be in your best interest to partner with someone who does; they would be known as a money partner.

Commercial loans: Commercial loans allow investors to purchase commercial properties. Not unlike traditional loans, commercial loans carry long durations. To minimize the risk of default, commercial loans tend to offer low interest rates. As a result, it may be harder to receive approval for a commercial loan.

Getting started in real estate investing is not as hard as you may think. If you’ve chosen your focus – i.e., single-family homes, apartments, commercial real estate, etc. – and your preferred exit strategy – i.e., flipping, buy and hold, or wholesaling – all that is left is finding the capital to fund your first deal. The importance of understanding real estate financing should not be overlooked because financing is what can help you turn your strategies into realities. Several lending sources are made available to those who are willing to put in the work, which is why “I don’t know how to finance a real estate business” is no longer an excuse to avoid investing.

Alternatives For Small Business

Small businesses looking for financing methods have more than a few options to choose from. If you own a growing company and need to keep reinvesting returns, check out the following alternatives:

Private Placement: A private placement is essentially a real estate syndication, but the business would take the role of project sponsor. In this arrangement, an unregistered securities offering is made directly to investors. The goal is to bring more equity to the current project.

Build-to-Suit: Build-to-suit is exactly what it sounds like. A commercial project is designed and built for the end user, it is then managed by an investor who manages the financing. In return, the operating business agrees to sign a long-term lease. While the business does not officially own the property in a build-to-suit arrangement, they do get long-term access to a custom build space.

Sale-Leaseback: A third option to consider is a sale-leaseback. In this arrangement, a property is sold to an investor and the business leases it back. Similar to a build-to-suit arrangement, the business will not own the property in the end. However, the money earned from the sale can then be funneled into a new development project.

6 Tips For Getting Property Development Loans

Acquiring money for property development may prove difficult for first-timers. Because the crash rate for property development is high, only experienced developers obtain loans easily. Follow these suggestions to help you overcome to difficulties of gaining real estate development loans:

Acquire Credibility: You should try to gain the experience needed to be trusted with a real estate development loan. This can be done by working for an established property developer, and in turn, they can give you this credibility.

Find A Partner: Partners can be useful if you already have some of the funds to begin with. If you find a developer to partner with, they will be able to co-finance with you.

Develop An Attractive Plan: Acquiring property development financing can be gained easier by creating an attractive project plan. Developers who are just starting usually look into small residential projects consisting of one or two homes. Property development loans can take up to months to obtain. In some cases, the property you want may be off the market by the time you receive a loan. Try to identify several different properties you may be interested in. Zoning limitations, access easements, utility easements, and other special conditions are all things you should research when developing a plan.

Do Your Research: Potential lenders will be more likely to offer you a real estate development loan when you provide an extensive amount of information about your project. Research the local property market to establish accurate sales prices and prepare any building cost estimates, including materials, labor, overhead, and profit.

Practice Your Pitch: Finally after all your planning is complete, begin rehearsing your pitch. Take all the information you’ve gathered and express it confidently, concisely, and convincingly. Be prepared to answer any questions about costs and the property itself. The more information you can provide them on the spot, the more your lenders will be willing to give you a property development loan.

Keep Costs Low: When it comes to property development loans, you want to keep all costs for the project low. The lower your costs, the higher your profits. If you can keep your development costs low, you benefit both yourself and any potential equity investors. You will also want to keep costs low if you are getting a property development loan from a bank. It is proven easier to secure funding for lower costs projects. When banks provide debt, they reference two numbers: the percentage of your total projected cost and the percentage of total projected value once the project is completed. As the repayment of this debt is very difficult during the development process, you will want to keep initial costs low. If anything goes wrong, banks will be unforgiving.

Best Real Estate Development Loans

When looking for the right real estate funding sources, it is important to weigh the costs, qualification requirements, speed of approval, and more. Aspiring investors should be careful to examine any variables involved in receiving real estate development loans to ensure they choose the best financing option for the situation at hand. The following list of real estate development loans is a great place to start:

US Bank: Loans provided through US Bank are a great option as they can allow investors to borrow up to 80 percent of the property value. Their loans can come with variable or fixed interest rates, and repayment terms can be up to 25 years.

Wells Fargo: Wells Fargo is one of the biggest real estate funding sources in the country. Investors may find they can be granted funds as quickly as four to six weeks when working with Wells Fargo. Additionally, they are less focused on borrowers’ credit when compared to other financing sources.

JP Morgan Chase: JP Morgan Chase provides real estate loans to several real estate investors each year, focusing on property types ranging from multi-family to mixed-use. One of the biggest benefits of working with this loan provider is the streamlined application and qualification process.

Liberty SBF: This lender is a great option for investors looking to borrow up to 90 percent of the property value. Their flexible loans will typically be made up of three portions, coming from a mix of traditional lenders, development companies, and your own down payment.

SmartBiz: SmartBiz works to match investors and loan providers based on the borrowers specific needs. Their loans are most attractive for investors seeking financing quickly, though the qualifications can be higher when compared to other loan providers.

4 Stages Of Real Estate Development

There are 4 stages of real estate development when looking at a standard development process. The first stage is choosing the right site and purchasing the land that you will be using for your development. The next step is to start planning your development as well as securing the permits and licenses required to build on the land. The third step is to start the development and construction of the project. The final step is to finish construction and start operating the development as you had planned.

Funding For Real Estate Investing: Which Will You Choose?

To find financing for real estate development, you must start by reviewing your strengths. The above options are almost always available, but you must understand what you’re getting yourself into before pursuing a particular strategy.

Regardless of what financing option or development loan you go after, all lenders will want to hear certain things. Be straightforward as you lay down the numbers and tell them what they can expect. Lenders will want to know your timeline, your expected profit, the loan amount required, when they can expect to see a return, and how involved you want them to be.

While it is important to appear confident in any meeting with a potential lender, it is most important to be transparent and gracious. Remember, the lender is helping you. Of course, they will benefit so long as the deal pans out the way you hope it to, but they are still taking a risk. Be ready to share your portfolio and answer any question a lender throws your way.

Summary

Financing a real estate deal is a very involved process. In fact, there are several real estate development loans designed to help buyers in every situation. If, for nothing else, everyone’s needs are different, and the loan options made available to borrowers suggest as much. As a result, borrowers need to shop around and confirm they are borrowing the right loan.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}