Bank Pull Back Creates Construction Lending Opportunity for Debt Investors

Building a property from the ground up entails substantially more risk than purchasing an existing building that is already generating income. Likewise, financing construction is riskier than lending against existingstructures since development projects don’t generate income to pay loan interest until they are completed. For this reason, most bank-originated construction loans come with additional restrictions to try to manage these risks. For example, when a bank extends a construction loan, borrowers usually don’t get all the cash up front. Instead, construction loans are disbursed gradually as portions of the development are completed and inspected by the lender.

But builders don’t have to borrow from banks. They can also borrow from investors that lend their own cash, and these “debt investors” or “investor lenders” have become more active in construction lending over the last three years.

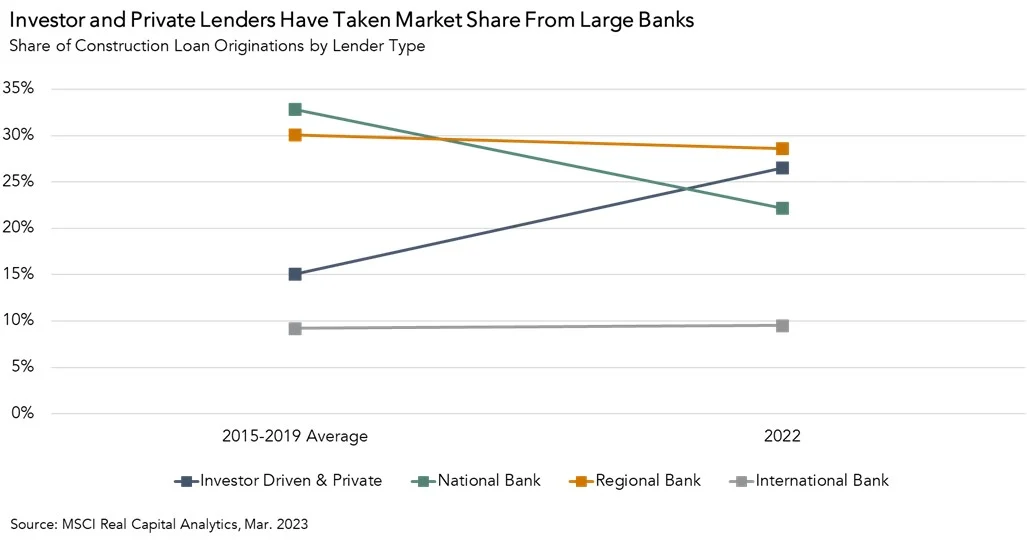

Investors Overtake Large Banks in Construction Lending

Traditionally, banks of all sizes were the most active construction lenders. However, during the pandemic, national banks meaningfully stepped back from construction lending, while regional banks stayed active. In the five years preceding the pandemic, national banks had the largest market share of construction lending. Now they’re in third place, outpaced by investor lenders and regional banks.

While the market share of construction lending for banks of all sizes still exceeds that of private lenders, investor-driven lending has clearly taken market share from banks over the last two years. Private construction loans are attractive to borrowers since they typically have fewer restrictions than bank construction loans. However, in exchange for the less restrictive debt, borrowers pay meaningfully higher interest rates.

With the potential for additional regulatory scrutiny on the horizon, U.S. banks of all sizes increased their cash balances by approximately $310 billion compared with early March. While some of this cash, approximately $98 billion, is due to borrowing from the Federal Reserve, most of it isn’t. If banks continue to hold onto more cash for risk management and regulatory purposes, there will be less cash available for CRE lending, especially for riskier varieties like construction financing.

Investor lenders may well continue to take share from banks. As they do, financing construction will become costlier.

Related Posts